GLP-1 agonists are already driving trend, more on the way

The explosion in popularity of GLP-1s will not come as a surprise to those sponsoring pharmacy benefits.

Leaving aside their newly approved use for obesity, accelerated growth in the utilization of GLP-1s for diabetes had already made them a top trend driver over the past few years. Given their glucose-lowering effects, GLP-1s have become standard of care for type 2 diabetes, supplanting other medication classes such as sulfonylureas.2 In 2023, GLP-1s represented 63% of diabetes spend, up from 38% in 2020.2

While diabetes GLP-1s will continue to account for a greater portion of spend compared to obesity, costs related to GLP-1s prescribed for obesity are expected to grow at a faster rate over the next 3 years. One consideration unique to covering GLP-1s for anti-obesity is that while plan sponsors will incur new short-term pharmacy costs, expected cost offsets such as lower medical benefit costs may not materialize until years later.

The promising obesity outcomes enabled by drugs such as Wegovy have prompted other drug manufacturers to pursue their own development efforts to help claim their share of this unprecedented market opportunity.

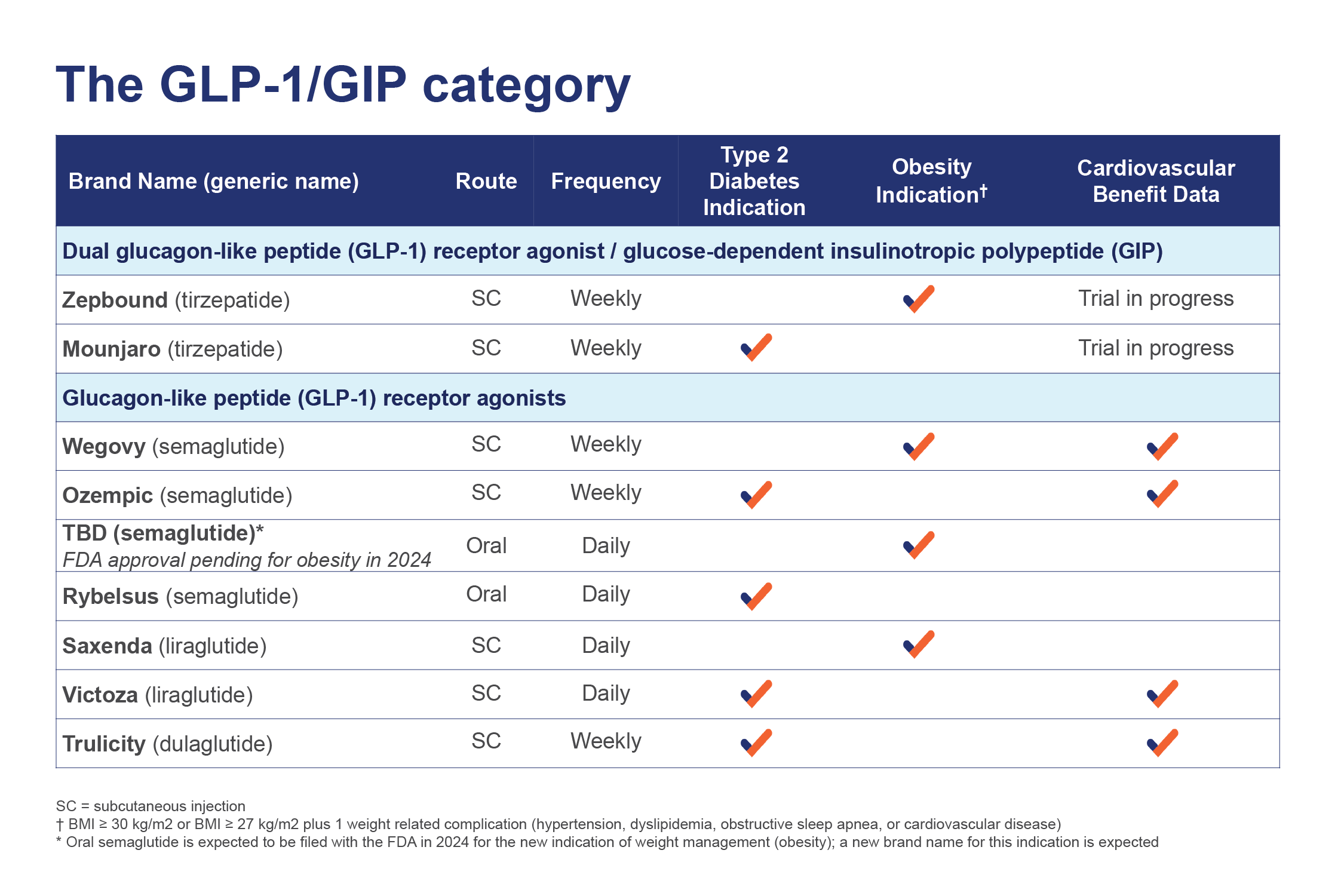

GLP-1 and GIP drugs and their indications

This chart shows GLP-1 and GIP drug class including route of administration, frequency and indications.